MARKET UPDATE

The market capitalisation of ASX Listed Investment Companies (LICs) and Listed Investment Trusts (LITs) finished 2019 above $53.1bn, a 12 month increase of 29.6%. During the quarter there were 3 new listings that raised a combined $2.3bn, with KKR Credit Income Fund (KKC) raising $925m. $272m was raised in secondary offerings and led by a Gryphon Capital Income Trust (GCI) entitlement offer that raised a $104m after raising over $122m the previous quarter, highlighting the strong investor demand to gain access to the Australian fixed income credit market which includes residential mortgage-backed securities (RMBS) and asset backed securities (ABS).

Ellerston Global Investments (EGI) was the top performing LIC/LIT with a net shareholder return of 24.1% in the December quarter versus a pre-tax NTA return (incl. net dividends) of 10.2%. During the quarter, the Board of EGI announced a proposal for an orderly conversion of EGI’s investment portfolio to an unlisted trust structure. Bailador Technology Investments Limited (BTI), which invests in private IT companies that are in the ‘expansion stage’ of their business cycle, provided a net total shareholder return of 17.9% and a pre-tax NTA (incl. net dividends) of 11.0%. This was predominately due to a 27% valuation uplift of BTI’s carrying value of the unlisted company SiteMinder.

TOP INVESTMENT PICKS

MFF Capital Investments Limited (MFF): Continued superior long-term performance

Global equity mandate that has provided shareholders with a net return greater than 20% p.a. (incl. dividends) over the past 10 years from investments that have attractive business characteristics at a discount to their assessed intrinsic values. The portfolio is highly concentrated with the top 20 holdings accounting for 97% of the portfolio, with Visa (16.3%) and MasterCard (15.6%) that largest holdings. We calculate MFF’s indirect cost ratio at ~0.41% as well as having a franking credit reserve of over $66m as at 31 December 2019. After December 2019, the current entitlement to a performance fee will be removed.

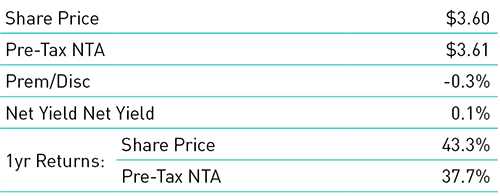

Global Value Fund Limited (GVF): Multi-asset discount capture

GVF invests globally using a discount capture strategy, owning a range of global assets purchased at a discount to their intrinsic value. GVF aims to provide an alternative source of market outperformance compared to more common stock selection strategies, identifying or creating catalysts that will be used to unlock the identified value The portfolio has an allocation of ~40% in listed equity. Based on the last close price of $1.075, GVF’s recently declared fully-franked FY20 interim dividend of 2.9cps provides an annualised net and gross yield of 5.4% and 7.4%¹, respectively.

Plato Income Maximiser Limited (PL8): Maximising income for SMSFs & pensioners

PL8 provides a well-diversified portfolio of Australian listed equites that aims to deliver shareholders with annual income (incl. franking credits) in excess of the S&P/ASX 200 Franking Credit Adjusted Daily Total Return Index. The Manager, Plato Investment Management Limited, achieves this by 3 means; dividend run-up effect, franking credits and running a dividend trap model. PL8 invests directly into a ‘no fee’ class of one of the Manager’s unlisted funds. Management Fees are 0.82% p.a. (incl. GST & RITC).