All sound with synergies coming online

PPS delivered a strong result, consistent with prior aspiration for double digit revenue growth and slight operational leverage. PPS does not provide net inflow guidance but mentioned it expects meaningful flows to follow the recent client onboarding. Things generally sound better with PPS now on track to realise +$3m run-rate EBITDA from OV before incrementing. Levers to achieving this include the final FTE synergies, and ending of the TSA, completed in Feb’25, providing confidence in the target.

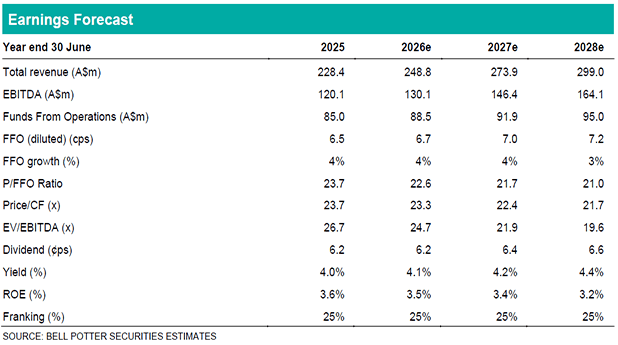

Financial highlights: Pro-forma revenue of $56.0m was up +5% on pcp against our $55.6m forecast with Platform revenue ex-churn from OV up +10% on pcp. Main call out was Spectrum revenue margins, which had a dilutive effect due to large account balances of early enterprise clients. Portfolio Services revenue of $10.2m declined by -3% on pcp. with the volume reduction offsetting some price benefits. We highlighted record volumes in the prior quarter, providing a recovery, and this was confirmed in the outlook statements, which guide to the full run-rate of portfolios in the second half. EBITDA of $15.2m was up +18% on pcp. PPS continued to exercise measured cost growth around mid-single digits and captured some initial synergies, the net effect of this driving outperformance against our $14.8m forecast. Below EBITDA line, items were broadly in-line with our thinking, where NPAT of $8.7m was up +11% on pcp.

Outlook: PPS has reissued an expectation for $9m in net salary cost reductions from the announced restructure, outlining tailwinds for operating expenses and capitalised costs. This is expected to see cash payments track back to the internal R&D levels of around $10m. Cost reduction remains the smallest opportunity in the opinion of PPS, relative to transformation in the technology offering and revenue growth. This is based on an improved time-to-market, internalisation of the superannuation administration

piece and greater relevance. OV churn has ceased with remaining assets transferred.

EPS: We make minor EPS changes to reflect some fine-tuning around the treatment of net salary reductions related to Technotia and D&A, modelling +2%/-2%/+1%.

Investment thesis: TP $1.20 (unchanged)

PPS offered little surprises and remains well placed to reinvigorate sales growth while making the operations leaner. Our Buy rating is unchanged and we continue to see an opening to achieve double digit revenue growth, amplified through cost-out measures.