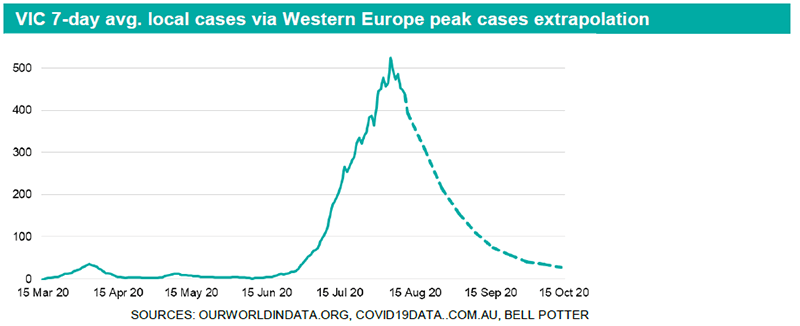

Western Europe suggests Victoria’s cases will continue falling

After analysing Western European data, their collective outcome suggests that Victoria’s lockdown measures will drive down its coronavirus cases (at least in the short-term). An extrapolation of the data points to Victoria’s current wave likely peaking on 5 August, and that its 7-day average local cases may fall to ~75 by ~mid-September. The analysis also suggests that Stage 4 lockdowns were not necessary to contain Victoria’s outbreak.

Australia may see a period of stability, but Europe shows fragility

With NSW so far seeing success at restricting growth in its outbreak, Australia may benefit from a period of stability in cases, particularly as it moves out of winter. Though despite supressing its first outbreak, Europe is now experiencing a 2nd wave, which calls into doubt the long-term sustainability of a severe suppression strategy, with continued lockdowns not a sustainable long-term solution. Impacts are already being seen in Victoria via huge spikes in crisis hotline contacts.

Regions adopting elimination strategy face indefinite isolation

The continued adoption of elimination strategies across Australian states excluding Victoria and NSW, risks permanent isolation from Victoria, NSW, and the world, and at the very least, the continued maintenance of strict 2-week quarantine requirements. This comes as the rest of the world gradually comes to terms with the inevitability of the virus’ spread. Past pandemics, such as the 1968 Hong Kong flu and 2009 swine flu virus’, continue to remain in circulation today. Herd immunity unfortunately remains the only way to normality, and areas that have adopted an elimination strategy face indefinite world isolation and as seen in NZ, continued risks.

Vaccine unlikely to be the magic bullet

Dr Fauci, Director of the US NIAID, recently stated that the chances of a potential vaccine being highly effective are not great, while the FDA has claimed a vaccine that is only 50% effective will be approved. Ineffectiveness would be in-line with the seasonal flu vaccine, with the CDC estimating it was only 29% effective in the USA’s 2018-19 flu season. As opposed to preventing infection, a potential vaccine will instead likely be touted as simply helping to control the spread.

Community sentiment crucial to predicting the pathway forward

The potential for further lockdowns, or a re-opening will ultimately be driven by community sentiment, which is likely to evolve over three key phases: 1) fear of the unknown and desire for severe suppression (or elimination); 2) gradual realisation of overall costs and lockdown fatigue; and 3) realisation of the inevitable outcome and drive for normality. China is currently in the 3rd stage, and has likely been there for some months, as the country fires up its economy and returns to normal. This will enable it to further cement its status as a world power, as other nations languish under restrictions. Much of the USA is now also in stage 3, with 9m new jobs created during the past 3 months as the nation re-opens.