Thanks to inflation and legislation that links certain superannuation caps and thresholds to the inflation rate, many retired and soon-to-be-retired superannuation members will receive a modest boost to their retirement savings. It is, in many ways, a case of giving with one hand and taking with the other.

On 28 January 2026, the Australian Bureau of Statistics published the December 25 inflation figures. As a result, the general transfer balance cap (TBC) is expected to increase from $2m to $2.1m on 1 July 2026. ATO confirmation is expected in March.

For those who have fully utilised their personal TBC, there will be no benefit. However, for those in the following situations, advice should be sought to help maximise the benefit:

- Are eligible but yet to start a retirement phase pension

- Have not fully utilised their personal TBC and have the potential to transfer additional amounts into the retirement phase

- Have a transition-to-retirement pension and will meet the full condition of release before 30 June

Will the contribution caps also increase?

While the general TBC increases with inflation, contribution caps increase in line with the Average Weekly Ordinary Time Earnings (AWOTE). The index values for the December 2025 quarter will be released on 26 February. Based on current expectations, from 1 July 2026, the annual concessional cap is expected to increase from $30,000 to $32,500, and the non-concessional cap from $120,000 to $130,000.

This will flow onto the other various linked caps, including the maximum non-concessional three-year bring forward rule of $390,000 and the concessional carry-forward allowance.

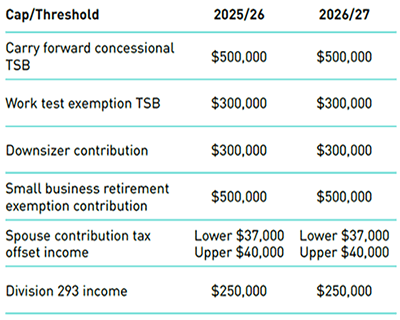

What is not indexed?

A lot remains unindexed. In fact, the direct link between inflation and the general TBC is relatively unusual. The caps and thresholds listed in the table below, among others, are hard coded into the legislation and therefore are not indexed with inflation or AWOTE.

Act now or delay

As 30 June approaches, indexation is likely to receive increased media attention. This often leads people to question whether they should delay starting a pension or completing a contribution strategy. So, the question remains – what should they do?

The answer is not a simple yes or no. A range of factors should be considered before making a decision, particularly around earnings and timing. These may include one-off income, the time remaining before 30 June, the unused indexation proportion, previous and future contributions, future eligibility to contribute and the potential crystallisation of SMSF-owned assets with large unrealised gains.

Next steps

As with most superannuation strategies, timing is critical. Now is the time to seek advice. Get in touch with your Bell Potter adviser for a more detailed discussion.

LEARN MORE

Our Technical Financial Advice team, in conjunction with a Bell Potter adviser can help you create a road map to achieve your financial goals, no matter where you are today. Whether you are looking for one-off advice or ongoing advice, our team can assist.

Get in touch with us to set up a complimentary initial appointment over the phone or in person across Australia.