Greater uncertainty, reduced market incentives

We have updated our gold price forecasts to reflect the greater levels of uncertainty that have manifested in financial markets and trade policy since the inauguration of US President, Donald Trump. We had previously considered the risks and implications of tariffs, but had not expected the rate, scale and pace with which they have been both implemented and removed. In addition, we had anticipated favourable corporate tax policy changes that would encourage investment and boost equity valuations. Instead, the uncertainty is hurting capital investment, sentiment and equity markets. It’s driving a flight to safety and the unencumbered value preservation offered by gold bullion. This has spurred a rally to all-time highs for the gold price in an environment where real interest rates remain elevated, and the US Dollar is at historically high levels. Either of these rolling over would provide a further tailwind for the gold price from current record levels. These factors are informing our forecast gold price increases.

Gold price forecast changes

We now forecast the following gold prices: 1HCY25: US$2,890/oz/A$4,634/oz (+7.1%); 2HCY25: US$2,950/oz/A$4,758/oz (+9.3%); CY26: US$2,800/oz/A$4,300/oz (+12.0%); CY27: US$2,700/oz/A$3,900/oz (+6.3%); and LT: US$2,800/oz/A$4,000/oz (+8.5%). These prices are in nominal terms. We have made no changes to our foreign exchange rate forecasts. Our near-term forecasts to end CY27 are within ±5% of the latest consensus. Our LT (long-term) forecast is 8% above the latest consensus.

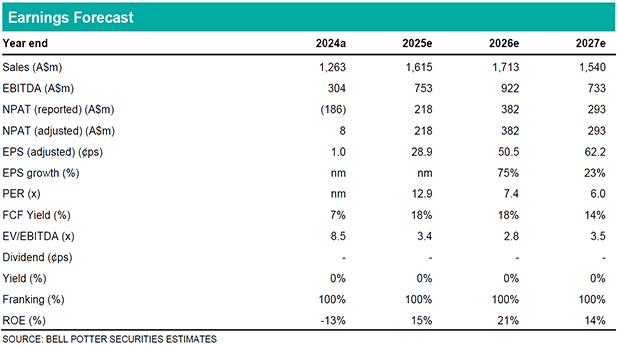

Investment thesis – Buy, TP $4.34/sh (from Buy, TP$3.75/sh)

EPS changes in this report are FY25: 20%, FY26: 44%, FY27: +44% on our higher gold price forecasts. RRL’s sensitivity to the gold price is among the highest in the large ASX gold producers. We are attracted to RRL’s all-Australian, multi-mine asset portfolio, its demonstrated leverage to the gold price, sector leading cash generation and its fully unhedged, debt free position. Our NPV-based target price is increased by 16%, to $4.34/sh. We retain our Buy recommendation.