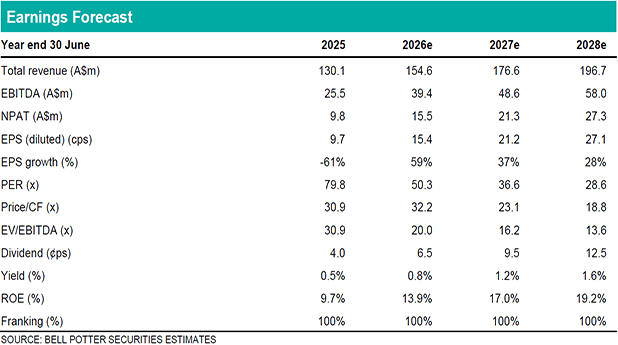

Revenue in line, narrow miss at EBITDA and NPAT

FY25 revenue of $130.1m was in line with our forecast of $130.3m while statutory EBITDA and NPAT of $25.5m and $9.8m were 2% below our forecasts of $26.1m and $10.0m. Cash flow was strong with a conversion ratio of 136% driven by a $7m reduction in working capital. Net debt at 30 June was $8.1m. The final dividend of 2.0c was below our forecast of 4.8c and the payout ratio on the total was 41%.

Weaker guidance on margin than expected

PWR does not provide guidance but in general terms said it expects revenue growth in FY26 for both Motorsports and Aerospace & Defence (A&D) – but stable or muted growth for OEM and Aftermarket – and “modest improvement” in the NPAT margin. We had forecast around a 550bp increase in the FY26 NPAT margin so this was below our expectations. PWR called out that the margin in FY26 was being impacted by US tariffs ($1.5m), US cyber accreditation ($0.8m) and CEO transition ($0.5m).

Downgrades

We have modestly downgraded our revenue forecasts in FY26 and FY27 by 3% and 5% largely driven by reductions in our OEM and Aftermarket forecasts. We have also downgraded our statutory EBITDA forecasts by 14% and 16% driven by the reduction in our revenue forecasts as well as a reduction in our margin forecasts. And we have downgraded our NPAT forecasts by 27% and 26% and now forecast an NPAT margin in FY26 of 10.0% (compared to 9.5% underlying in FY25).

Investment view: PT down 3% to $7.75, Down to HOLD

We have increased the multiples we apply in the PE ratio and EV/EBITDA valuations from 35x and 17.5x to 45x and 20x and also reduced the WACC we apply in the DCF from 9.4% to 9.2% given the outlook remains positive but the margin recovery is taking longer than we expected. The net result is a 3% decrease in our PT to $7.75 which is only a modest premium to the share price so we downgrade our recommendation to HOLD. In our view the stock is looking reasonably priced on an FY26 PE of c.50x.