“Just when I thought I was out, they pulled me back in”

NST have downgraded FY26 guidance for a second time this FY, just when we thought NST were seeing light at the end of the tunnel. Gold sales are now expected to be at or around 1,500koz down from the previously revised 1,600-1,700koz

guidance (BPe 1,601koz, VA 1,614koz prior to the downgrade). The reasons driving the downgrade primarily stemmed from KCGM mill throughput challenges with intermittent outages in the float circuit and electrical issues compounding downtime. Throughput over the remainder of the year is likely to average ~9Mtpa vs the initial 12Mtpa FY26 guidance. Adding insult to injury, productivity at Jundee continued to disappoint with grades failing to meet expectations and prompting a shift in resources to higher-margin operations. Management reaffirmed AISC guidance of A$2,600- $2,800/oz, however on our assessment this is likely to be pulled potentially at the 3Q result. Total group gold sales across Jan-Feb were 220koz (2QFY26 348koz), we have pared back our estimate for KCGM, adjusting throughput to 7.4Mtpa (annualized) in 3Q and 10.4Mtpa in 4Q at an average grade of 1.8g/t. We remain sceptical on the throughput grade required to meet the updated guidance, given mined grades are tracking around 1.6g/t and being delivered for processing through the new Mill in FY27.

Strike through FY26, focus on FY27

Management have effectively drawn a line through FY26, choosing to prioritise commissioning and operation readiness of the upgraded plant. We sense that NST may look to carve out expensive, capital hungry operations like Jundee, in time, however noting that our estimate of value (~A$5bn) may be a bitter pill to swallow for some.

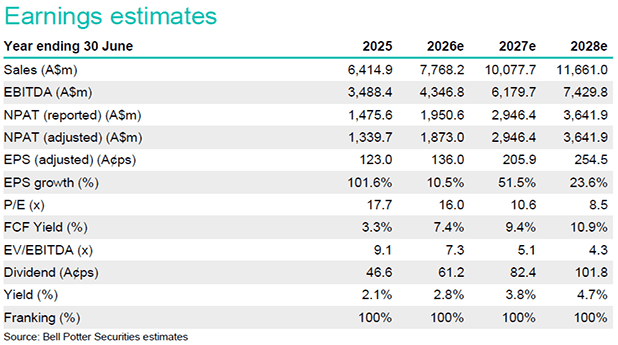

Investment thesis: TP $35.00 (unchanged)

Our Target Price is unchanged at $35.00/sh, and we maintain our Buy recommendation. The disappointing downgrade however is likely to remain as a significant overhang for the stock over the next 12-18m until the ramp up of the upgraded mill at KCGM commences. We see potential positives from asset rationalisation, given the high capital and operating costs at the likes of Jundee and Thunderbox. EPS changes in this report are: FY26 -16%, FY27 -10%, FY28 0%.