Sulphur price risk considerations

We note reports of increased sulphur pricing and potential supply constraints emerging due to the conflict in the Middle East. Primarily produced as a by-product of petroleum and natural gas refining, approximately 25% of global production is sourced from the region. Production disruptions and shipping restrictions (much of exported supply is shipped through the Strait of Hormuz) have led to supply concerns and price spikes from ~US$250/t to US$500/t. Sulphuric acid (produced from sulphur) is a substantial input into the High Pressure Acid Leach (HPAL) nickel production process, requiring ~8-10t of sulphur per tonne of nickel produced. NIC produces its own acid on site, from elemental sulphur, accounting for ~40% of HPAL production costs. We understand NIC’s HPAL operations have ~2-3 months of sulphur stocks on site.

Earnings impact limited by diversification, leverage

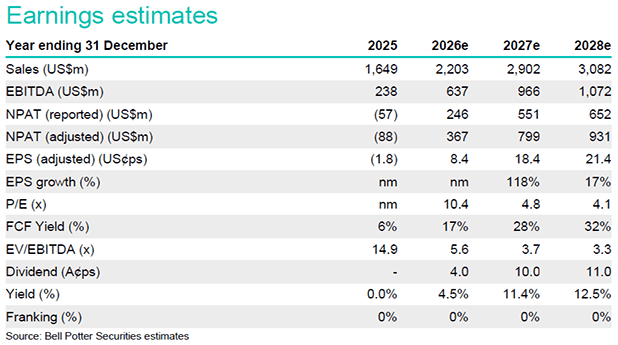

On our prior modelled assumptions, incorporating a doubling of the sulphur price into our CY26 forecasts results in a ~15% (US$100m) cut to our consolidated EBITDA forecast, to US$571m. We still forecast that NIC would meet its debt service obligations and have capacity to pay a (reduced) dividend. NIC continues to benefit from its diversified nickel production base, with the Hengjaya Mine (HM) and the Rotary Kiln Electric Furnace (RKEF) operations not exposed to sulphur input costs. There is scope for input cost inflation here (via diesel and Indonesian thermal coal) but to a lesser extent, as price increases have been more moderate and subject to mitigating factors including fuel subsidies and adequate supply. We point out that if we include a positive response (5%) in the nickel price that may flow from production constraint concerns, this would more than offset higher sulphur costs. When incorporated into our high sulphur price scenario, it results in a net 4% increase in EBITDA (attr.) compared with our prior base case.

Investment thesis: TP $1.45 (unchanged)

While the conflict in the Middle East is resulting in an immediate market impact to key input costs and the duration is uncertain, we form the view that while margins may be impacted, NIC is insulated due to its diversified nickel product suite. There is also a potential offset from higher nickel prices to which NIC has strong leverage. We retain our Buy recommendation and leave our $1.45/sh Target Price unchanged.