Company background

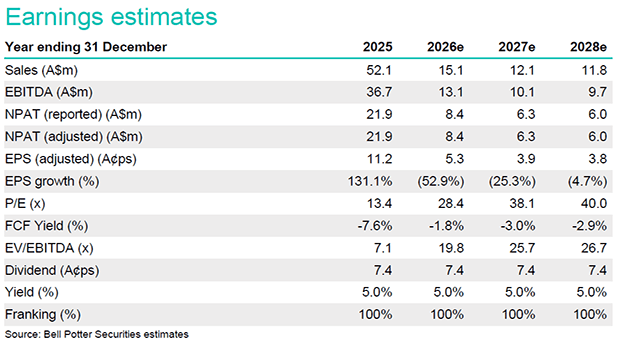

Rivco Australia Ltd (RIV) is an ASX listed entity providing investors with exposure to the Australian water market. As at Feb’26, RIV held a portfolio of 58.8GL of entitlements (portfolio NAV of $1.79/sh pre-tax and $1.62/sh post-tax) with an ~80% bias to High Security (HS) water assets (by value) on the Southern connected Murray Darling Basin (SMDB). RIV generates returns through: (1) the leasing of entitlements (53% of the portfolio is under lease with a WALE of 3.2 years at Feb’26); (2) the sale of annual surplus allocations received against the entitlement position in the spot market; and (3) the disposal of long-term entitlements above carrying value. Having been established in 2016 as an externally managed vehicle, RIV has recently internalised the management structure which should result in a material reduction in operating costs moving forward, reducing the management fee leakage that had been prevalent in years past. We initiate coverage with a Buy rating and $1.65/sh target price.

Attractive through the cycle returns

Over the past decade SMDB entitlements have delivered average annual cash yields of 3.5% p.a. and capital returns of 10.0-12.0% p.a. with periods of outperformance tied to permanent cropping development. Over the past five years capital returns have been more modest, however, a period of Government buybacks (~160GL over 5yrs and 230GL slatted for purchase) and modest expansion in tree nut planting (+1.3% p.a.) may trigger a return to higher levels of capital growth.

Investment thesis: Buy, TP $1.65/sh

RIV enters FY26 with the highest level of contracted revenue and available allocation in five years supporting a positive near term earnings outlook. In addition, with rising lease rates (+40bp YoY and 5-6% implied yields in current market offers) we see the scope to lift the portfolio return as leasing and re-leasing opportunities emerge (which should emerge as a theme from 2H28e). At the asset level, we see the shift in aligning future dividends with operating earnings as potentially moving group strategy to sustain and grow the asset base, acting as a catalyst to bridge the gap to NAV (post-tax NAV of $1.62/sh and pre-tax NAV of $1.79/sh).